Usual Solution To Home Mortgage Questions

Article created by-Svenningsen KlintA lot of people are so willing to jump at the first home mortgage they find that they end up getting burned by an unstable, variable loan. This is obviously something you want to avoid and thus you need a good understanding of how the industry works. Below, you will read some great tips pertaining to home mortgages and how you can get a good loan.

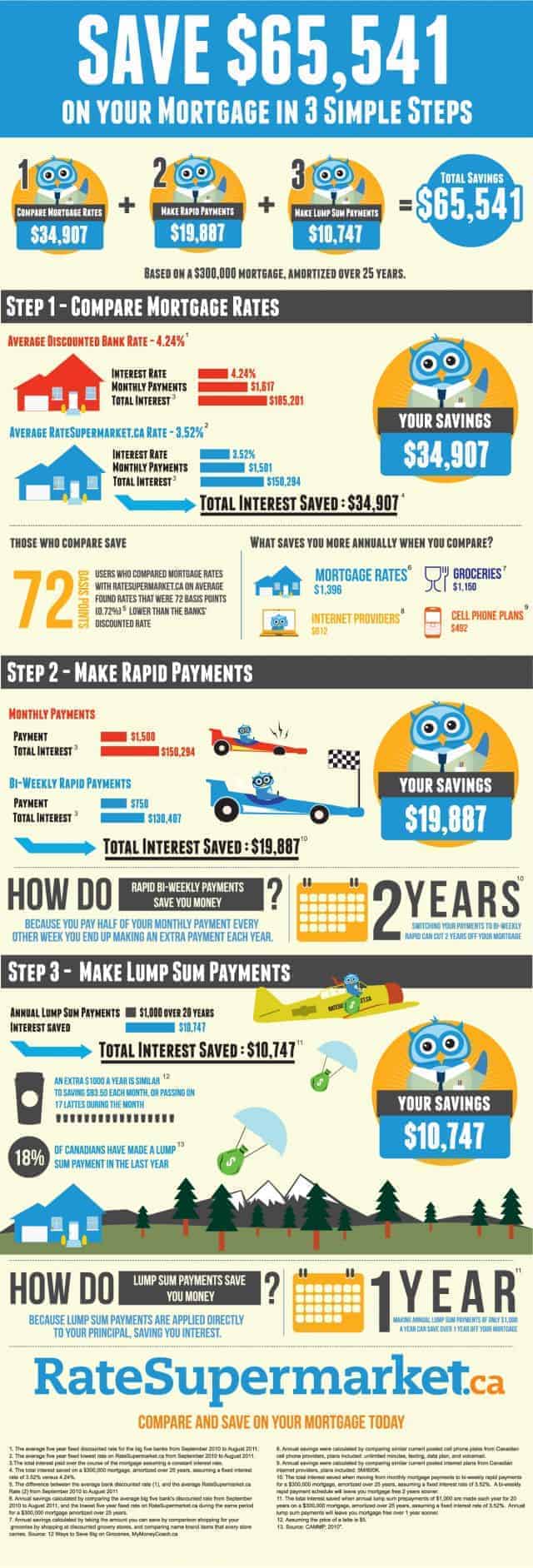

Before trying to get a mortgage approval, find out your credit score. Mortgage lenders can deny a loan when the borrower has a low credit score caused by late payments and other negative credit history. If your credit score is too low to qualify for a mortgage loan, clean up your credit, fix any inaccuracies and make all your payments on time.

Remember that the interest rate isn't the most important part of a mortgage. You also have to think about closing costs, points and other incidentals. There are different kinds of loan as well. That is why you have to find out as much as you can about what you're eligible for.

If you are a veteran of the U.S. Armed Forces, you may qualify for a VA morgtage loan. These loans are available to qualified veterens. The advantage of these loans is an easier approval process and a lower than average interest rate. The application process for these loans is not often complicated.

A fixed-interest mortgage loan is almost always the best choice for new homeowners. Although most of your payments during the first few years will be heavily applied to the interest, your mortgage payment will remain the same for the life of the loan. Once you have earned equity, you may be able to refinance your loan at a lower interest rate.

What do you do if the appraisal does not reflect the sales price? There are limited options; however, don't give up hope. You can dispute the appraisal and ask for a second opinion; however, you will need to pay for the appraisal out of your pocket at the time of the appraisal.

Pay down your debt. You should minimize all other debts when you are pursuing financing on a home. Keep your credit in check, and pay off any credit cards you carry. This will help you to obtain financing more easily. The less debt you have, the more you will have to pay toward your mortgage.

A good credit score is essential if you want to finance a home. If your score is below 600 you have some work to do before you can hope to purchase a home. Begin by getting a copy of your credit record and verifying that all the information on it is correct.

Know that Good Faith estimates are not binding. These estimates are designed to give you a good idea of what your mortgage will cost. It should include title insurance, points, and appraisal fees. Although you can use this information to figure out a budget, lenders are not required to give you a mortgage based on that estimate.

If you have filed for bankruptcy, you may have to wait two or three years before you qualify for a mortgage loan. However, you may end up paying higher interest rates. The best way to save money when buying a home after a bankruptcy is to have a large down payment.

Remember, no home mortgage is "a lock" until you've closed on the home. A lot of things can affect your home mortgage up to that point, including a second check of your credit, a job loss, and other types of new information. Keep your finances in check between your loan approval and the close to make sure everything goes as planned.

Avoid a home mortgage that has a variable interest rate. If the economy changes, your rates can go through the roof. This could result in you no longer being able to afford your home, which you, of course, do not want to see happen.

https://www.wsj.com/articles/farmers-in-crisis-turn-to-high-interest-loans-as-banks-pull-back-11573381801 require a home to be inspected before the loan is approved. Although this costs a small amount of money, it can save you thousands in unknown expenses. If the home inspector finds problems with the home, you have the opportunity to either negate the contract or to renegotiate the sales price.

Never assume that a good faith estimate is fact or written in stone. It is in fact not just an estimate, but one written in good faith. Always be wary of extra costs and fees that can creep into the official and formal paperwork later that drive up your total expense.

Understand what happens if you stop paying your home mortgage. It's important to get what the ramifications are so that you really know the seriousness of such a big loan as a home mortgage. Not paying can lead to a lower credit score and potentially losing your home! It's a big deal.

When rates are near the the bottom, you should consider buying a home. If you do not think that you will qualify for a mortgage, you should at least try. Having your own home is one of the best investments that you can make. Quit throwing away money into rent and try to get a mortgage and own your own home.

Increase the amount that you pay each month if you get a higher paying job or a substantial raise at work. Do not waste the money on expensive nights out, clothing, cars or other toys instead. Your home is one of your best investments, so treat is as such.

There are times when the seller of a home will be able to give you a land contract so you can purchase the home. The seller needs to own the home outright, or owe very little on it for this to work. A land contract may need to be paid within a few years.

When the bank asks a question, be honest. It is a terrible idea to lie when applying for mortgage loans. Never misstate assets or income. If you do you could find yourself saddled with more debt than you can actually afford to pay. It may seem good in the moment, but in the long-run it will haunt you.

Now you know how to get a great loan without any headaches or stress. As long as you use the tips you've read here, you should have no problems in the future. Be go now to use this education so that you don't stumble over the hurdles the experts who wrote it have already dealt with.